" transform="translate(9 6)" width="6px"/></svg>)

Is Property Investing Out Of Reach For The First-Time Investors?

So, you’re considering property investing. You must be feeling proud, for you have successfully saved an amount of money to put into a big investment; and excited, for the possible…

So, you’re considering property investing.

You must be feeling proud, for you have successfully saved an amount of money to put into a big investment; and excited, for the possible return the investment will bring; and, most probably, nervous, for this would be the first time ever you are putting so much money in one thing.

“Maybe I’m not ready for property investment yet?” You might be thinking.

Don’t worry. Property investment is not out of reach for first-time investors. We have helped so many new investors, who earn an average salary and don’t have astronomical amounts in their savings account, successfully purchase high-quality investment properties with decent returns, taking them one step closer to financial freedom.

Property Investment is not as hard as you may think if you understand the four facts below.

Look across the country to generate the greatest outcome

Fast price and rental growth can occur in affordable areas.

You can afford a decent house with an average salary.

It is not difficult for the rental income to cover your costs.

Of course, it’s not convincing by just listing them. We are now going to explain each fact in detail.

Look across the country.

You may think that a house is too expensive, especially if you are a “Sydneysider”. However, if you look at other cities rather than making the most common move (compromise for a cheaper apartment in your backyard) there are plenty of affordable options.

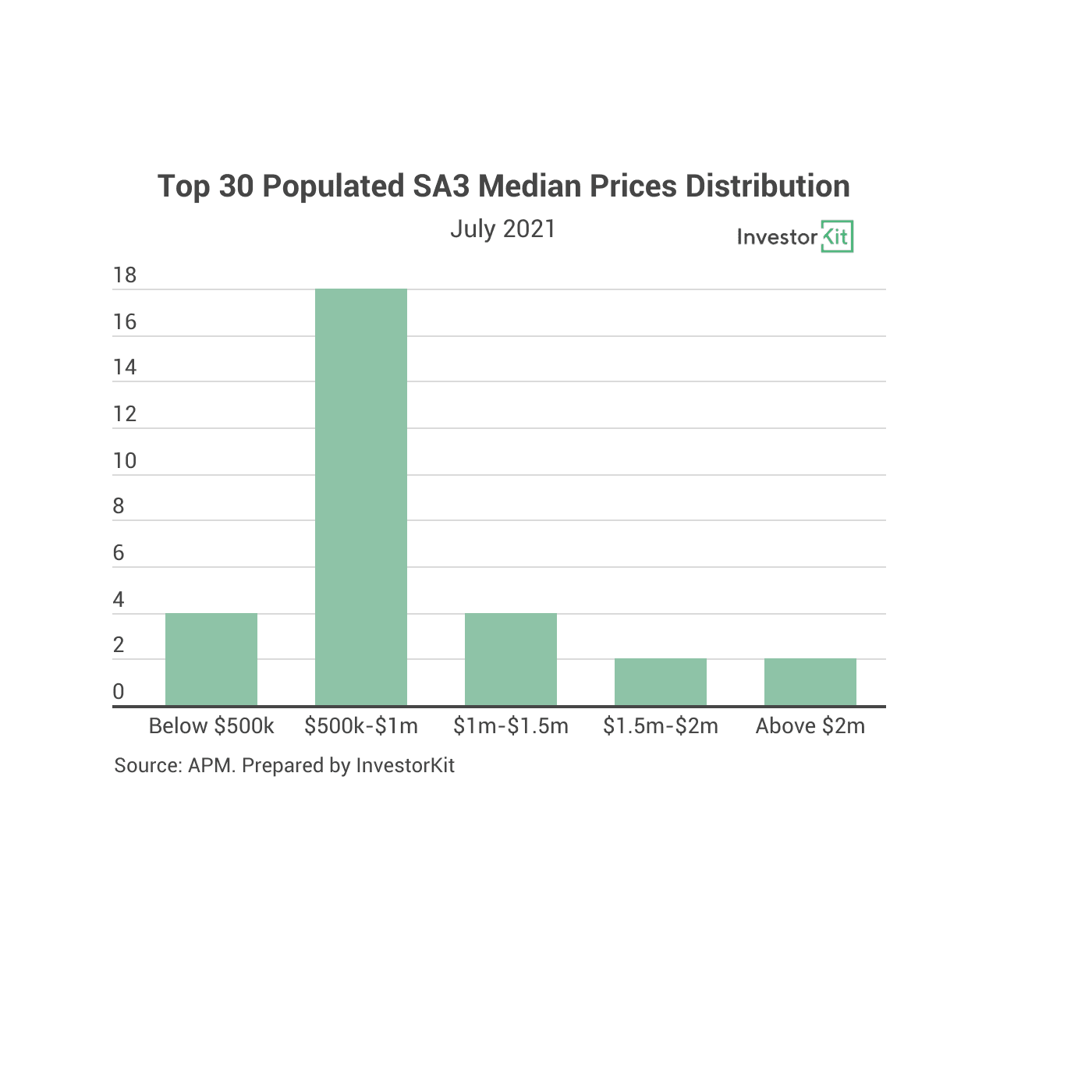

Let’s first look at our many towns across Australia. I have listed the Top 30 most populated ABS Statistical Areas Level 3 (SA3) below.

Note: SA3s are often the functional areas of regional towns and cities with a population more than 20,000 or clusters of related suburbs around urban commercial and transport hubs within the major urban areas.

Admittedly, we see extremely high median house prices above $1million in the most populated SA3s (which sit in our capital city sub markets), some with more than $2million. However, if we dig deeper..

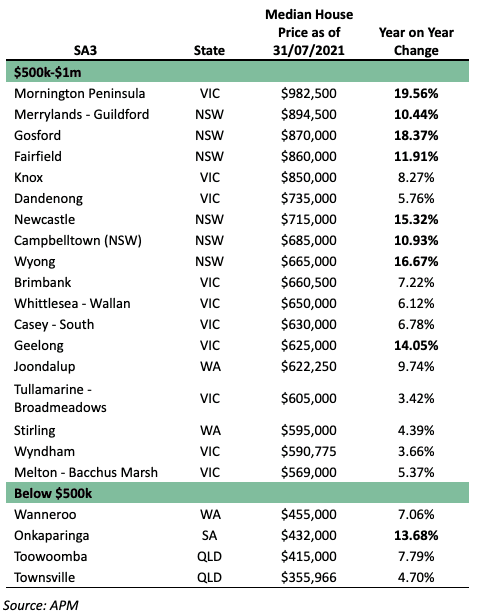

22 out of the 30 most populated SA3s have a median price below $1million. Four of them are even below $500k!

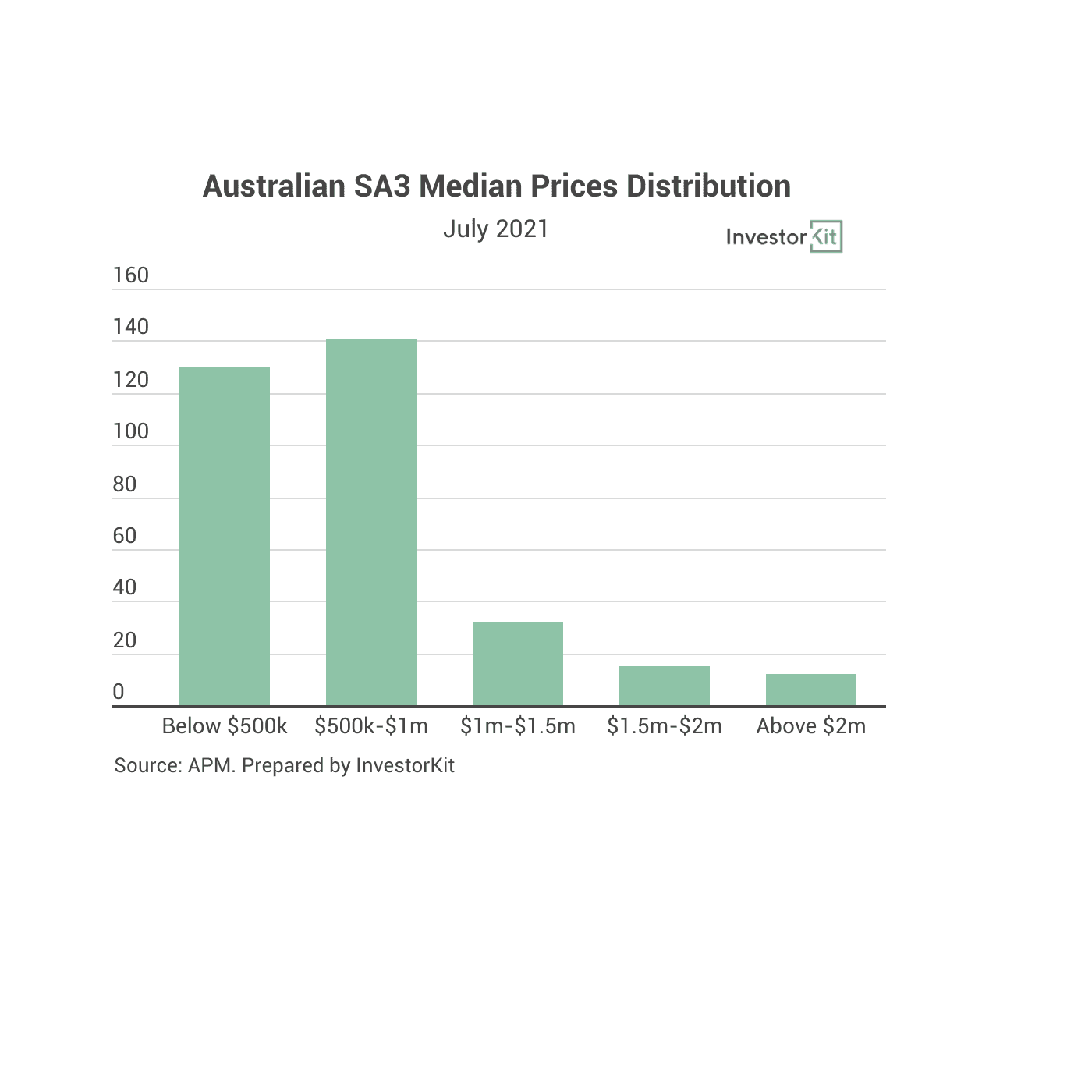

How about the bigger picture? Let’s look at the median price distribution of all SA3s of the country.

82% of Australian SA3s still have a median price below $1m, and almost half of them are under $500k. Smaller SA3s have contributed more to the affordable price range.

Please note, although we are using population to define town size here, population or its growth should not be the most important factor affecting your decision on where to buy. Here is why.

2. Fast price growth occurs in affordable areas too.

Many assume that a property which carries a lower price point, is often inferior and in turn will not have a great amount of appreciation. This is very far from the truth.

When thinking that way, you might have forgotten that a market is self-regulated, meaning that when the house price of one area is too high to afford, it pushes demands to other locations and pulls the house prices up. History shows that our lower priced markets on many occasions have had growth rates to a similar trajectory as our higher priced markets. Fun fact, corelogic 2011-2021 median house price growth rates of Campbelltown and Newtown were similar, even with Newtown now being close to 3x as expensive. Many also would agree that Newtown is a very desirable place to live in with all its amenities/appeal and distance to the CBA. However, these desires don’t necessarily create a greater outcome.

It’s not just a theory. In our blog Why Stations, Schools, Shops, Beaches and Distance to CBD should NOT be Your Number One Focus when Investing, the data analysis shows that there was very little growth variances between suburbs in a similar area that had all “the good stuff” to those that did not.

Let’s have a look at the Year-on-Year growth of the Top 30 populated SA3s with under $1million median prices.

9 out of the 22 SA3s have achieved double-digit annual growth, 5 of which have a median house price lower than $800k.

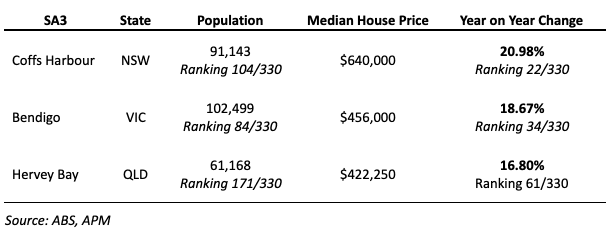

And again, this Top 30 populated list is just an example. You don’t want to limit yourself to the most populated cities when looking for great performers. Plenty of cities with much smaller populations are performing well. Here are some examples:

3. You can afford a decent house with even just an average salary.

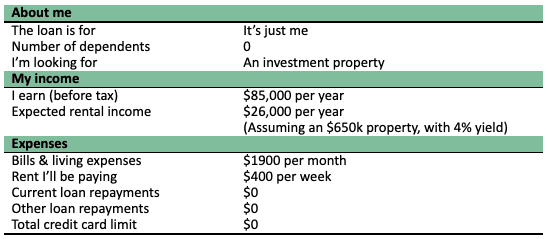

Not sure if you can afford an investment property all by yourself? Let’s see how much an individual can borrow with an annual salary of $85,000 before tax.

We used the Commonwealth Bank’s Borrowing Power Calculator with some basic assumptions around various expenses to conduct the calculation. The below table shows our inputs.

Based on the above inputs, you may be able to borrow up to $600,300 from CBA (*subject to change as banks update their calculators). If borrowing 90% of the purchase price, you will be able to buy a house that is worth up to $667,000. Let’s just round it down to $650k.

According to APM market data ending July 2021, that figure, is higher than the median house price of 180 Sa3 regions which equate to approximately 55% of all SA3s across the country.

4. It is not difficult for the rental income to cover your costs.

Now that you have got a loan to repay and a property to take care of, do you have to sacrifice your life quality for them? The short answer is no. It is essential that the house sustains itself and doesn’t put any extra burdens on you. Is that hard to achieve? Let’s check.

Yield is the annual gross rent expressed as a share of the total purchase price. Usually with a yield of 4% or higher, the rental income can cover your costs of holding the property with an interest-only loan. Considering the loan interest rates are so low lately, we can even lower the benchmark to 3%. Interest rates won’t stay low forever, this is where rents will change and so should your buffers.

If you look at the yields of some centric areas of Sydney and Melbourne, you would be frustrated by how low they are. To give you some examples, by the end of July 2021, Sydney’s Eastern Suburbs – North Sa3 region recorded a 1.62% yield, and Melbourne’s Stonnington – West recorded a 1.55% yield, the lowest across the country.

However, the next-to-CBD suburbs of Sydney and Melbourne are never your only choice. If you look at regional cities or just other capital cities, yields there are much more favourable.

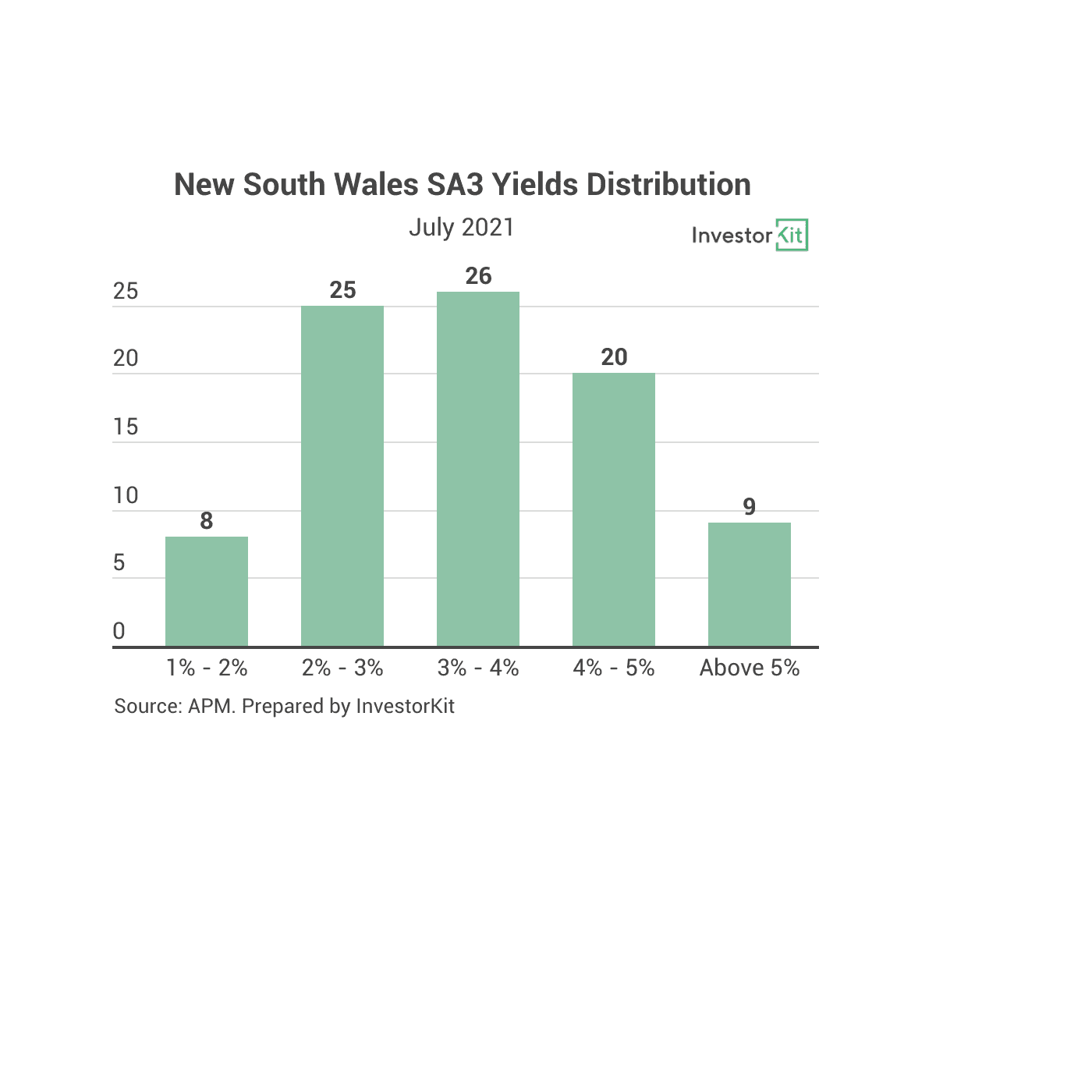

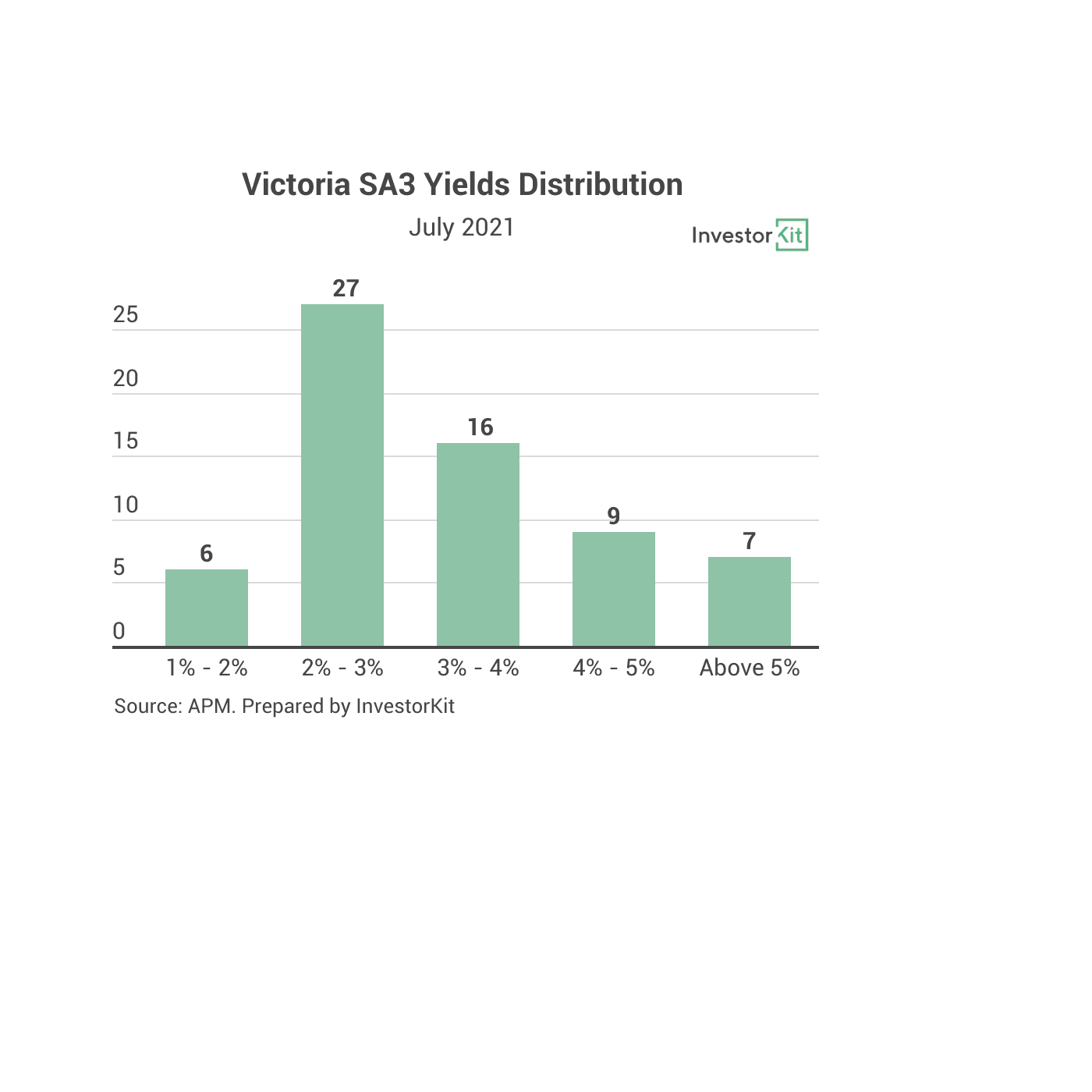

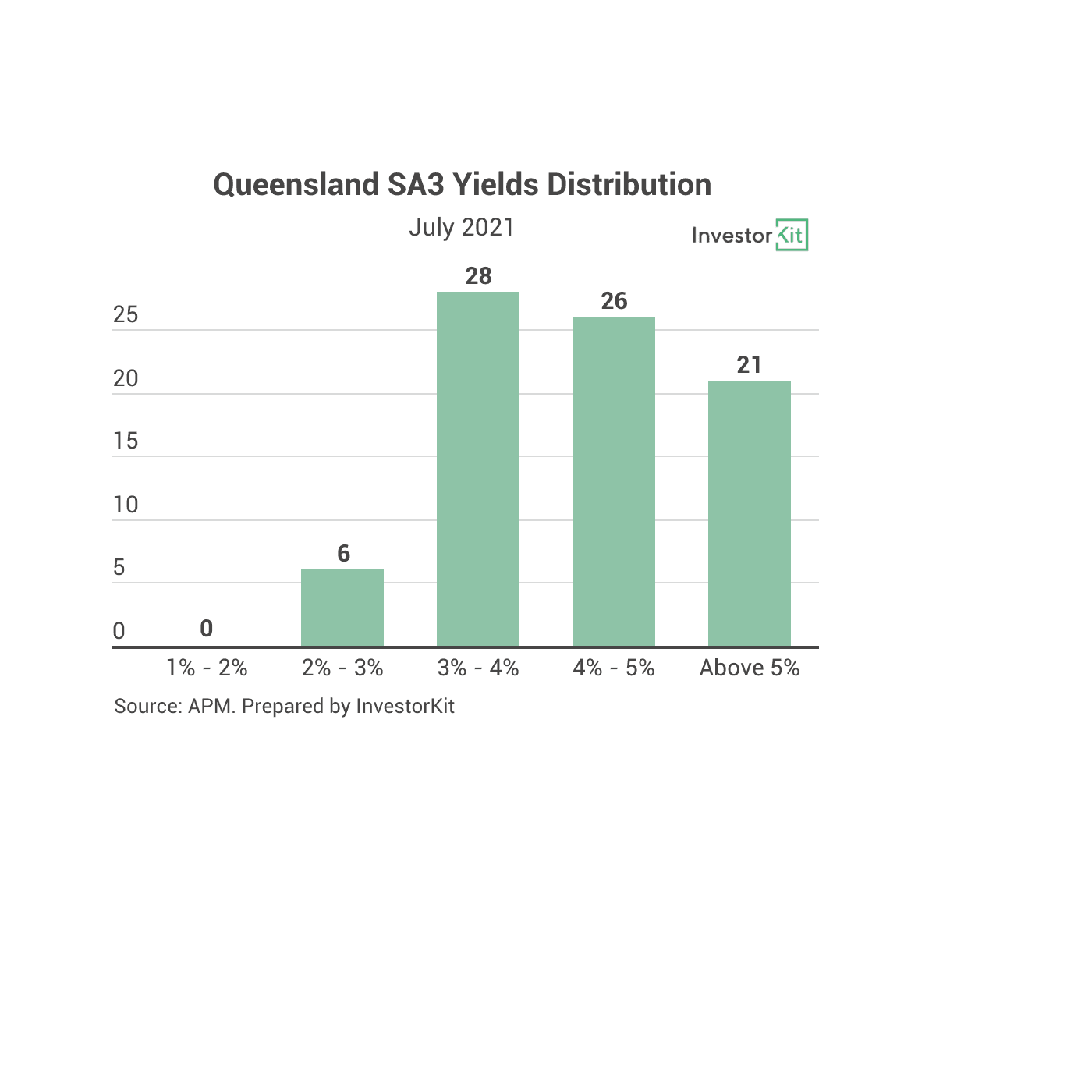

The below charts show the distribution of house rental yields in New South Wales, Victoria, and Queensland. You can see that although the rental yields of Sydney and Melbourne houses are low, there are plenty of SA3s in the two states that have a figure higher than 4%. In the Sunshine State, most of the SA3s are still enjoying high yields.

A few moments ago, we learned that with a salary of $85k per year, you can easily afford a $650k property. Let’s check how SA3s meeting that budget are performing nationwide.

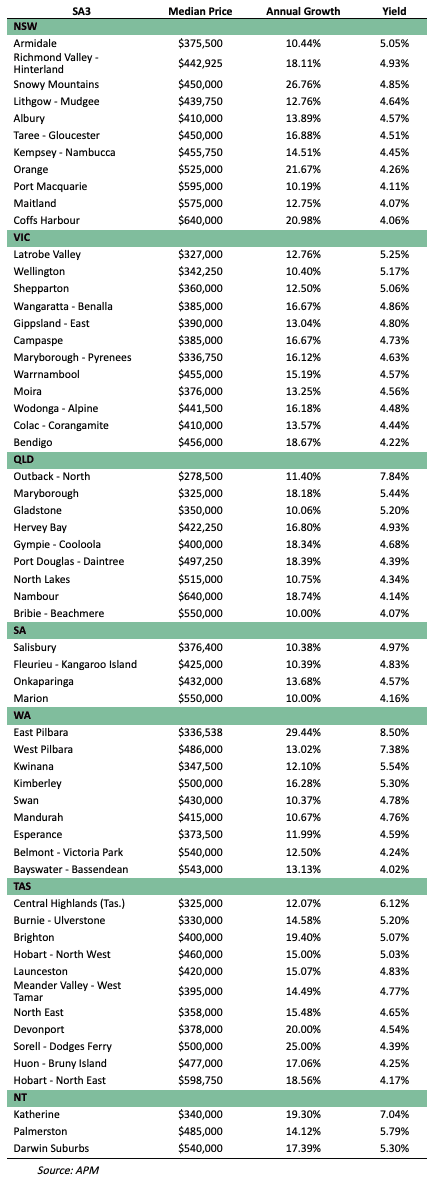

We searched for SA3s with a median house price under $650k that achieved double-digit annual growth in the previous year, and a 4%+ gross rental yield. You know what? We got 59 of them! That is almost one fifth of all. Below is the list.

We must admit that some of the above areas are not suitable to really buy and hold a property in due to their lack of employment diversity or their lack of statistical reliability. This only applies to a small amount of the above regions. (want help from our buyers advisory team to find the right regions? get in touch HERE!). However, it has proven that it’s not difficult to get your cost covered with a smaller budget and at the same time achieve a strong growth in value if you are putting your money in the right place.

Data has demonstrated that successful property investing is not out of reach for a first-time investor if you understand that there are plenty of locations across the country where the price is affordable, strong growth is happening, and the rental income is sufficient to cover the holding costs. The key is to identify these locations and put your money in with the right timing.

The impressive performing cities we have discussed about today are only some of the locations where InvestorKit and our clients have been purchasing in and benefiting from in the past few years.

Curious about how we identify the locations and which locations are worth buying in now? Don’t hesitate to book a 45-min FREE no-obligation discussion and start your property investing journey today!

Keep Reading

" transform="translate(5 5)" width="14px"/></svg>)